|

am sure the thought of retirement has crossed your mind in the past. The media is awash with stories of relatively young people retiring early and admittedly I have found myself envying some of them. Whilst retirement may mean different things to different people, our definition of retirement slightly different. It is freedom from a 9 to 5, an ability to live life on your terms and chase your “true” dreams, be it traveling or for that matter starting up a business. Would it not be nice to be on your own boss and not having to worry about foregone income from an active job?

The classical wisdom is to work hard for upwards of 3 decades for most people, save diligently in IRA’s or other tax advantaged accounts and hope to have enough of a nest egg after those long years of hard work. Albeit, the classical wisdom is also a big lie propelled by Wall Street. The two big reasons why the classical wisdom fails you are: Inflation and Volatility. With the kind of currency printing that has been happening in the US (and all over the world really), it is easy to intuit that cash will basically be trash, if not already. Money printing in the US it not new, the Fed has been printing money for quite some time now. But, 2021 took things to a new level. 40% of all the available US dollar supply was printed in the last 12 months alone! This is a staggering fact that has implications on asset valuations and more importantly accelerating erosion of cash sitting in bank accounts. The other reason why stocks/IRA investments don’t really work is because of the fact that the investments can and have been historically volatile. Imagine someone retiring in 2008 only to see upwards of half of their stock holdings evaporate (in the 2008 mortgage induced crash). Admittedly it was a horrible time. But the fact remains that stocks are volatile and often one has no control over such investments. The US does seem to have a bit of a “Retirement Crisis”. The NRRI or the National Retirement Risk Index measures the percentage of working age households that are at risk of not being able to maintain their pre-retirement standard of living. And the results are abysmal. The NRRI estimates that about 50% of those households will struggle in their retirement, you heard it right, 50%! Why do multi-family apartments shine on both those fronts? Real estate, especially yield producing real-estate acts as a natural inflation hedge. Why is that? Well rents are tied to inflation and often outplace inflation, apartment valuations are a close function of their income producing potential (rents). Yield producing assets also tend to fare better on the volatility front. In-fact over the previous 4 decades or so, investments in Real estate have proved to be significantly less volatile than stock investments according to a detailed study conducted by the Federal Reserve of San Francisco (The Rate of Return on Everything – 1870-2015). Arguably, someone with a well balanced exposure to yield producing Real estate would have fared much better in the 2008 recession. Apartments continued to thrive during that period as it was not the case that demand for housing went down. In-fact quite to the contrary it went up, as people lost their single family homes they needed a place to live. A lot of them chose to rent and apartments was an obvious choice. The Data shows this also. Apartment rents remained robust through the 2008 mortgage crisis despite the seismic storm in the single-family home market. Do you want to de-risk your retirement? Investing in multi-family is a great way to do that!

0 Comments

All investments are risky but some are riskier than other. As investors, maximizing your risk adjusted return is of paramount importance. All things equal, multifamily real estate offers a superior risk-return trade off and while the probability of losing one’s principal in such an investment is low, its not zero. There could be circumstances that could cause one to partially or in a rare case completely lose one’s capital. One of our main goals is to educate our investors about those circumstances and how to guard against those. Here are top reasons why an investor may lose money in a Real estate syndication:

1. Bad Operator: There are a lot of respected syndicators out there and by corollary there are also some bad actors who bring a bad rap to the entire community. Choosing a bad operator is a sure shot way to lose money. Some of the ways one can mitigate this risk is to carefully understand what kind of experience do the general partners bring to the table. Prodding questions seeking information about their exits, track record and their management practices can go a long way to ensure your capital is protected and moreover earns a respectable return. We cannot over-emphasize the last item which is around asset management. Here are Zovest, one of the ways in which we are building value for all our investors is to move towards self-management. We have come to realize that self-management is the one of the best way to reduce operational expenses and operate our assets in a lean fashion. A lot of syndicators rely on third party management and while there are some excellent property management companies, there are some unethical one’s as well. For us, controlling our destiny is of paramount importance which is why we are moving towards self-management. 2. Bad Underwriting: This is a bit subtle and is related to the point number 1 above. Make sure that you look carefully into all assumptions the general partners are making especially around rent growth and cap rates at exit. Any underwriting can be coaxed to say a story which may not be necessarily a story that is true. Here at Zovest, one of our main goals is to under-promise and over-deliver. We ensure that we err on the side of being conservative and use lower than expected growth assumptions in all the markets we operate in. Our goal is to ensure that we place a stringent risk lens on on all our prospective deals and stress test our assumptions. A deal has to jump through several hoops for us to be serious about it let alone launching it on the platform. 3. Bad Market selection: Real estate is all about markets and sub-markets. Make sure to ask questions about how the general partners select their chosen markets and sub-markets. Conduct independent research on those markets and validate their assumptions or debunk them. Another lens which is going to be increasingly important going forward is climate risk. A lot of sunbelt markets such as the ones in Texas and Florida are popular investment targets but they are also prone to extreme weather, especially around the coasts. We operate in Kansas city and most recently in Des Moines, arguably two of the strongest markets in the mid-west. In general we love the value mid-west brings. At the same time, both Kansas city and Des Moines are growth markets which are reasonably immune to extreme weather fluctuations. 4. Bad market conditions: Bad market conditions is another one. Real estate is an asset class that is exposed to the vagaries of local and global macro-economic climate. Real estate is also a cyclical asset class that goes through boom-bust cycles. Market conditions can potentially create strong headwinds that can cause a great investment to under-perform. One cannot influence the market but as operators it behooves us to deploy efficient risk management strategies to better weather adverse economic conditions. David Swensen (Yale endowment fund) was arguably one of the great world’s money manager (David passed way recently unfortunately). For people who don’t know the name, please check his wiki here (https://en.wikipedia.org/wiki/David_F._Swensen). Under David’s leadership, the Yale endowment fund produced returns in excess of 20% from 1988 to 2008 turning $1 billion into almost $23 billion before the financial crisis hit in 2008. That is exceptional performance not only because of what he was able to achieve from a return standpoint, but more importantly due to the consistency. Often as investors we tend to overlook the risk of any particular investment in search for “better” alternatives. Often a higher return means “better”. That is a wrong way to look at it though. What is crucially important is risk adjusted performance or returns adjusted for risk. This is where Swensen shined. Not only did he not produce a superior return but he did so very consistently.

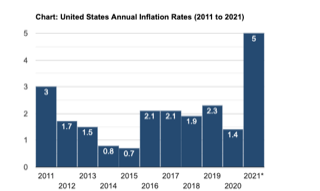

One wonders how was he able to do it? David was a big fan of alternative assets, of which real estate was a big component of his investment thesis. Swensen target portfolios allocated 10%+ to Real assets (including REITS). Some of the advantages of real estate investing include diversification, low correlation with conventional asset classes and a natural inflation hedge. In the more recent times, the Yale endowment fund has a shockingly low allocation to US stocks. Please check the article below: (https://www.barrons.com/articles/yale-endowment-only-2-percent-u-s-stocks-51630535033) Average retail investor participation in real estate is much lower than what Yale/Swensen recommend (~2% according to some recent surveys we conducted). How much of your portfolio is allocated to Real estate? If you have been paying attention to the asset markets in the last 12 months, you would agree that we have noticed some some significant but unexpected changes. While everyone predicted markets to crash, stock prices and real estate have boomed, to the contrary. Fast-rising housing costs have helped to push inflation to a 13-year high. But the way that government statisticians track the price of consumer goods may be missing just how explosive home-price growth has been in recent months. Altogether, the rise in housing prices accounted for over a quarter of the overall increase in inflation in May, a reflection of how heavily government economists weight this spending category. Consumer prices jumped 5% just in May of 2021 . They accelerated at their fastest pace in nearly 13 years as inflation pressures continued to build in the U.S. economy. Used cars and truck prices continued their climb higher, rising 7.3% in the month of May'21 and 29.7% for the past 12 months. The new vehicles index increased 1.6%, its biggest-single month gain since October 2009 and was up 3.3% for the 12-month period, the highest move since November 2011. Although the prices have been increasing, the wages have not increased much. As the country recovers from pandemic, rising inflation could attract federal reserve to raise the interest rates in near future. All in all my question is , how safe is holding cash if the money continues to loose value at this rate? Real Estate is one asset class where inflation works in our favor, with inflation, rents increase as well as property valuations, effectively hedging the risk of capital to a significant extent.  All of us perhaps have been watching the craziness in the real estate market. Home prices have seen an unprecedented surge across the country. The index of home prices across 20 large markets surged 12% on a yearly basis this past February, according to the S&P CoreLogic. Buyers have resorted to aggressive tactics in the market and there have been reports of offers made all cash, sight unseen and often with inspection and other contingencies removed. One wonders if this trend is supported by economic fundamentals or is a bubble in the marking? The word bubble does scare us as it brings the horrors of the 2008 crisis, which emanated and in the end destroyed the housing market.

One could be tempted to assume that the inflation home prices are seeing makes for a real estate bubble. We argue that is not true. In fact if you talk to any real estate expert, they will tell you the same thing. Real estate across the US is on fire, no doubt, but there are some very strong fundamental reasons behind the trend. Reasons that have been exacerbated by the COVID pandemic but have been at play before the pandemic. Housing if viewed as a commodity has to be driven by supply and demand and the equilibrium price is where the supply meets the demand. Housing in the US is in an extreme shortage. The supply of new homes reached a new low earlier this year (~2 months, or a number which represents how long it will take to sell out of new supply). Furthermore the pandemic has caused disruptions in the global material supply chains leading to a surge in cost of construction (lumber and steel). Combined with a low interest rate environment, this makes for a perfect storm in the housing market. These are some of the reasons we think that the surge is “not” a bubble. In fact its rooted in some rather large economic forces at play. How may this affect the multi-family apartment market? Rather closely actually. The market for single family homes is a very closely related cousin of the multi-family apartment markets. Similar forces affect both the markets. While you may not read a lot about that in the media, there is an unprecedented surge in the valuations in the apartment market as well, due in part to the very same reasons elucidated above. In summary, real estate is not in a bubble, at-least not yet. The surge may continue or temper in the coming months, we don’t know. Albeit, there are fundamental reasons behind the surge. This makes the bubble theory not applicable at-least in our opinion. What do you think? The COVID pandemic has caused unprecedented economic and emotional destruction. Lives and livelihoods have been lost all across the globe with many of the livelihood losses permanent. We hope that mass vaccinations campaigns underway in the US will go a long way in terms of building herd immunity and finally bringing an end of the biological crisis. Albeit, there is another crisis whose end is not so near and one which may just be rearing its ugly head. That crisis is inflation. Central banks all across the globe and especially in the US have pumped trillion of dollars in the economy. That jolt was needed to push the economy back on the path of recovery. However, they say there are no free lunches in economics. One of the downsides of this unprecedented amount of spending is a risk of inflation.

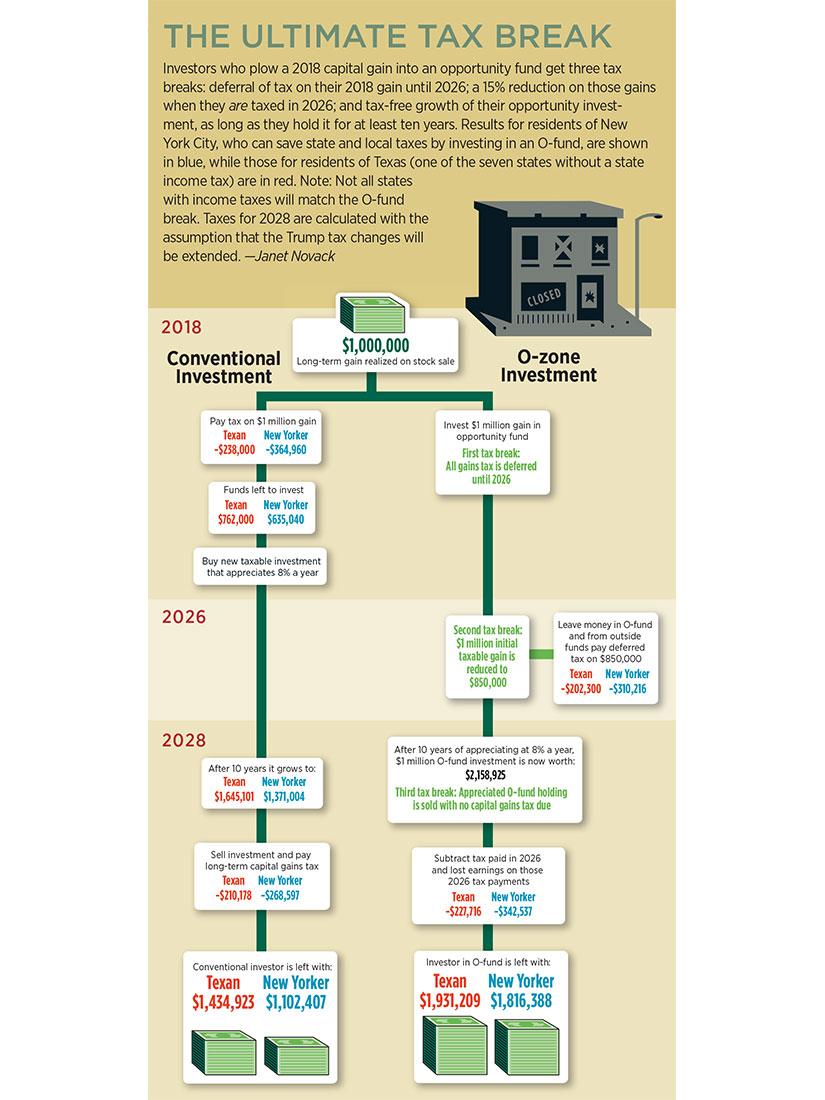

What is inflation? Inflation in simple terms is a rise in prices of good and services in the economy. Loosely speaking when there is an imbalance between the amount of money and the goods and services that the money chases, often it leads to rising inflation. The surge in money supply as a result of the Fed spending has that balance heavily lopsided right now. If for anything, a testament to the theory of rising inflation has been a surge in bond Yield we saw in the recent weeks. The price of a bond (or any fixed income instrument) is negatively correlated with inflation as inflation eats into the real purchasing power. Yields move inversely with prices and with the rising fear of inflation, have been climbing up in the recent past. Why is inflation a risk? One wonders what inflation has to do with real estate especially income producing real estate. Real estate of often touted as one of the best inflation hedge plays out there. Why is that? Its rather simple to understand that. Income producing real estate derives its value from its income producing potential or rents. Rents are very strongly correlated to rising inflation and typically outstrip inflation in terms of their year over year increase. As rents increase, the value of income producing real estate tied to those rents also increases. Some indirect ways of increase are related to a rising cost of replacement in an inflationary world. Simply speaking, it costs more to build and replace the asset. Rising inflation often has a pretty dramatic impact on the valuations of income producing real estate. While time will tell how high inflation rises to in the US or the magnitude of its impact, it sure is a clear and present danger. We opine that now may be a great time to diversify into income producing real assets, which as we discussed, are structured to do well in an inflationary world. Opportunity zones – What are they? According to the IRS an Opportunity Zones (OZ for short) is an economically distressed community where new investments, under certain conditions, may be eligible for preferential tax treatment. OZ’s were added to the tax code under the Tax cuts and Jobs act under the Trump administration in 2017. Investors need to invest in a qualified investment fund, which is a special purpose investment vehicle, or a Qualified Opportunity Fund (QOF) designed to invest in a qualified OZ (QOZ). OZ investing, if and when done right are a phenomenal way to shield capital gains, especially given the recent stock market appreciation. The common perception that OZ projects happen to be markets and sub-markets in decline isn’t true either. The COVID pandemic has dramatically changed the OZ landscape and there are some truly compelling opportunities in OZ’s! Opportunity zones – Tax advantages · Defer capital gains on recently sold assets until the earlier of the sale or the exchange date of the QOF investment and Dec 31st, 2026 a.k.a 1031 on Steroids · 10% exclusion on the deferred gains on a QOF investment held for 5 years or more · 15% exclusion on the deferred gains on a QOF investment held for 7 years or more · No capital gains on the OZ investment after 10 years by virtue of a stepped up basis Opportunity zones – Things to be mindful for

Opportunity zone – Recap We found the following schematic to be a good representation of the high-level workflow when it comes to OZ investing. Please check it out here.  We answer many questions to our first time and also existing investors. We want to take some time to list most frequently asked questions here. We will improve this blog post overtime to include more and also some pictures/ videos to understand the Apartment Syndication world better.

1) What is real-estate syndication? Syndication is a way to create a structure to pool money to buy an apartment building. Typically, we have GP’s (general partners) who are deal sponsors and LP’s (limited partners) who are passive investors. The GP’s conduct the due diligence, bring the deal to the LP’s and raise the equity required to close the deal. They also manage the asset on a long term basis. 2) Do you invest in your own deals? Absolutely we do! We invest anywhere from 5% to as high as 20% equity in the deal. Also, bear in mind that the initial capital needed to pursue the deal is ours and is at highest risk. We can lose all that money. Also, we guarantee the loan. Hopefully, you can see that we have enough skin in the game. 3) Who is an accredited investor? Regulation D of the SEC (Securities and exchange commission) act of 1933 defines an accredited investor as (OR)

4) Do I have to be accredited to participate in an offering? Not necessarily. Our offering typically fall in two SEC regulated exemptions, 506b and 506c. While a 506c offering is limited only to accredited investors, a 506b is not. 5) What kind of returns can I expect and how do you calculate them? Good question, especially given that there are a lot of different ways to measure performance. Our typical cash on cash return (the yield on your cash investment) range from 7-9% (varies from deal to deal). Our AAR (average annual return), which simply is the total return on your investment divided by the hold-time typically ranges from 16-20%. You may have heard of IRR or Internal rate of return which is yet another metric for measuring return. An IRR simply measures the rate of return you would sustain while staying invested in the project. An IRR is typically a better measure of performance and looks at both the cash flow and the time of investment, albeit is slightly more complex than the AAR. We do publish IRR’s metrics as well for all our projects. 6) What are your investment minimums? 50k is a good benchmark to go off of, although the minimums can change (go up for a particular deal). We like to start with a reasonable minimum to give folks a chance to participate. 7) What is your hold time? Typically, we shoot for an average hold-time of 5 years. This could go up or down depending on market conditions. 5 years is overall a good ballpark which gives us enough time to execute our forced value strategy as well as leverage principal pay-down, in order to get a superior equity multiple on the investment. 8) What are the investment risks? All investments carry risk, anyone who says otherwise does not know what they are doing, in our opinion. Real estate investments are also risky and are subject to a host of macro-economic factors. Albeit, multi-family apartments esp class B product in select US mid-western markets have demonstrated extraordinary resiliency to major economic storms, such as the 2008 mortgage crisis as well as current pandemic related economic damage. There is a lot of data that supports that claim and at a high level it is connected to a strong demand for rentals across the US, a perennially low interest rate environment fueling asset valuations as well as a under-supply of class B apartments in the US. We would be happy to talk in detail about these macro-variables and share data and reports corroborating these claims. 9) When will I get paid? We do quarterly payouts which are typically direct deposits into the investors account. 10) How often do you communicate? We send monthly updates on the investments progress. We share data on current execution plan progress and other performance metrics. As always, we are always happy to answer questions so as to ensure that you continue to be comfortable and happy with your investment. 11) What are the tax-implications of an investment like this? Real estate is a tax advantaged investment. The cash on cash return that we generate is shielded by depreciation often resulting in a paper loss. There are strategies for deferring gains on capital on the asset sale (1031 exchange). We suggest talking to your CPA to leverage these strategies fully. 12) What is a sensitivity analysis? We want to conservative in our forecasts and show investors what factors that can cause our performance to be better than our expectations or worse. A sensitivity analysis elucidates these range of outcomes. Often the variables that can cause these fluctuations are outside our control, albeit we try our level best to influence what we can. 13) Can I use a SD-IRA (Self Directed IRA) or solo 401K to participate? Yes, please check out our blog on this: https://www.zovest.com/blog/ira-401k-to-invest-in-apartments 14) What happens in the case I want to liquidate my investment? The investment should be considered an illiquid investment. That said, we understand that life happens. We will consider each request in its own merit and will attempt to best accommodate you. 15) What fees do you charge? Typically we charge 1% acquisition fee (on the gross asset value) and anywhere from 1-2% on the management side (on the gross rents). Our fee are meant to compensate us for the time/risk we outlay as we bring these investments to you. To you health and wealth, Zovest Team Risk and return go hand in hand. Typically return expectations of investors increases as risk of the investment increases. Investors seek to reduce the risk by diversifying across industries, asset classes and investment horizons. Whilst diversification is a great way to reduce portfolio risk, often times macro events which cause drastic and severe corrections. The 2008 mortgage crisis was a classic example of that. While the crisis emanated in the housing market, the contagion spread to most public markets in the US and worldwide almost causing a collapse of the US financial system. Nonetheless, the power of diversification cannot be understated regardless of portfolio size and composition.

What makes a portfolio diversified: Knowing the benefits of portfolio diversification, one may ask what makes a portfolio diversified. The key idea behind portfolio diversification lies in “correlation”. Correlated investment themes tend to perform similarly. By virtue of that, they would tend to do well under similar conditions and on the flip side do poorly under certain other conditions. One can achieve portfolio diversification by investing in assets that have low to a zero correlation among each other. Swensen’s 20% rule and Real estate’s superior diversification potential: The 20% rule created by David Swensen, the Chief investment officer at Yale endowment is a popular portfolio risk mitigation strategy and calls for allocation 20% of the portfolio towards alternative investments – one’s that have low correlation with traditional and publicly trades asset classes as as stocks and bonds. We argue that Real estate happens to one of the best choices to achieve near complete portfolio diversification. Some of the top reasons are: 1. Correlation advantage: Real estate has a low correlation with stocks and bonds. Historically the correlation has been as low as 0 in the early 2000’s to as high as 0.8 during the mortgage crisis. The average correlation across the previous 4 decades has been around 0.3 or so. This is great news from a portfolio diversification standpoint. 2. Inflation advantage: Real estate acts as a natural inflation hedge. Inflation hedge investments are investments that are expected to increase or at-least maintain their value over a period of time. The most typical example of that fact is the rising rental rates in most major sub-markets in the US. The sheer shortage of housing and the home affordability crisis has further caused an upward pressure on rents. 3. Illiquidity and market inefficiency: Real estate is an illiquid investment. While that fact could be construed as a negative, there are studies conducted that demonstrate the fact that retail investors don’t make money over the long run in liquid markets. This if often attributed due to “market-timing” tendencies of retail investors and quite to the contrary Real estate’s relative illiquid nature helps more than hurts. Illiquidity often also leads to market inefficiencies which sophisticated market participants can exploit. To your health and wealth! Zovest Team It is often said that Real estate is not a “get-rich quick” scheme. Whilst we agree with that, it surely is a “get-rich consistently” scheme. What do we mean by that? Well, consistently investing in Real estate can produce some stellar effects. It takes times to build the momentum but once the flywheel is up and running, it sure as heck runs! And if one is smart about it, one can program the flywheel to keep on running without putting in a lot of effort or even no effort.

It is illustrative to look at some numbers. The attached spreadsheet walks through one hypothetical 10 year investment horizon and showcases the power of real estate investing. First, some assumptions: We assume that every year we initiate a fresh investment amount of 50k, a cash on cash yield of 8% on any investment and a 16% annualized return realized at exit. Please note that these numbers are very typical of the offerings we bring to our investors. Monthly cash flow is calculated as an 8% yield on the cumulative investment (net worth) in any given year. For instance, in the first year one starts with 50k leading to an annual cash flow of 4k (50k*8%) and a monthly cash flow of $333.33. As time passes and as one’s investment amounts grow, the monthly cash flow and the net worth grows. For instance, in year 6 the monthly cash flows stands at $2333.30 and the net worth at 300k. Here is where the magic happens now!. Come end of year 6, the investment we made in year 0 matures and so does our net-worth. In year 7, we invest 50k as usual but we get a 100k bump from that exit leading to a cash flow of $3000 and a net-worth of 400k. This repeats in the subsequent years as we reap the fruits of our investments. By the time year 10 ends, we stand at a monthly cash flow of $5000 and a net-worth of 800k! In the same phenomenon, If you invest 100k per year instead of 50k, at the end of Year 10, you will get 10k per month of cash flow and Net worth of $1.6 MM. Now, that is some snowballing! The question is if you are ready to take that first step. We cannot wait! Take the calculator for a spin and give us feedback. To your Wealth! - Zovest Team |

Archives

November 2021

Categories |

RSS Feed

RSS Feed